Global capability centers (GCCs) in India were built on a simple premise: save money.

They were considered the “holy grail,” enabling companies to scale production while leveraging the unique strengths of different geographies:

- Lower salaries

- Cheaper real estate

- Follow-the-sun operations

But over time, that narrative began to shift.

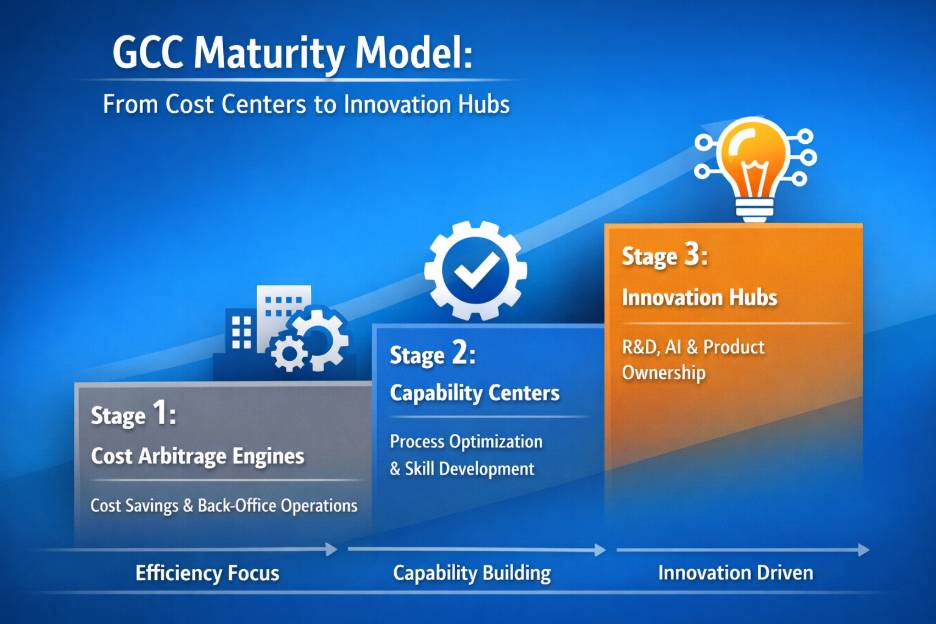

GCCs in India — long considered a “cost-efficiency” lever — became brain centers, harboring innovation, thinking, and problem-solving. Our blog puts this transition into the spotlight, unpacking the steady rise of GCCs in India into spaces where products are built, initiatives are led, and decisions shaping business outcomes are made.

Why GCCs Started in India?

The original logic was simple.

India had a vast pool of English-speaking, technically trained talent capable of leading initiatives from the ground up. Salaries were a fraction of what companies paid in the US, UK, and Europe. And with time zone differences working to their advantage, teams in Bengaluru could seamlessly hand off work to counterparts in New York.

At the same time, employment opportunities grew in countries hosting GCCs, contributing to broader economic growth. So, it struck a balance that worked for all.

Through the 1900s and 2000s, companies established GCCs as low-cost centers, primarily suited for IT support, finance and accounting, data processing, and back-office operations. The kind of work that was predictable, repeatable, and didn’t need to sit at headquarters.

GCCs were treated as cost lines. Their success was measured in how much they reduced the parent company’s expenses and not in how much value they created. That framing is almost unrecognizable today, and GCCs are now positioned as strategic, high-value innovation hubs for R&D, AI, and global operations.

From Support Units to Global Centers: What Really Changed?

There’s a clear rebalancing of expectations in view. Enterprises are no longer asking what GCCs can execute, but what GCC can own. This change in perspective around GCCs was shaped by three primary drivers:

- Talent Depth: India produces over 1.5 million engineering graduates every year. But beyond volume, the quality of talent matured. Engineers who started in support roles moved into architecture and became an integral part of core decision-making. A generation of professionals who grew up inside GCCs started leading them, enabling a culture of co-creating.

- Digital Infrastructure: India has a flourishing digital infrastructure, a defining catalyst for GCC growth. Cloud connectivity, high-speed connectivity, and a thriving startup ecosystem turned India into a promising geography for global execution and innovation. Bengaluru alone has over 940 startups operating alongside GCCs, creating a cross-pollination effect that Silicon Valley would recognize.

- Strategic Necessity: The pandemic exposed uncomfortable truths about global companies: they had fragile, HQ-dependent decision-making models. When everything went remote, the GCCs in India didn’t just keep running, but ran better, ensuring continuity through strong digital infrastructure, distributed teams, and round-the-clock operations. That gave Indian GCC leadership a seat at the table they’d never had before.

How Big is the GCC Ecosystem in India Right Now?

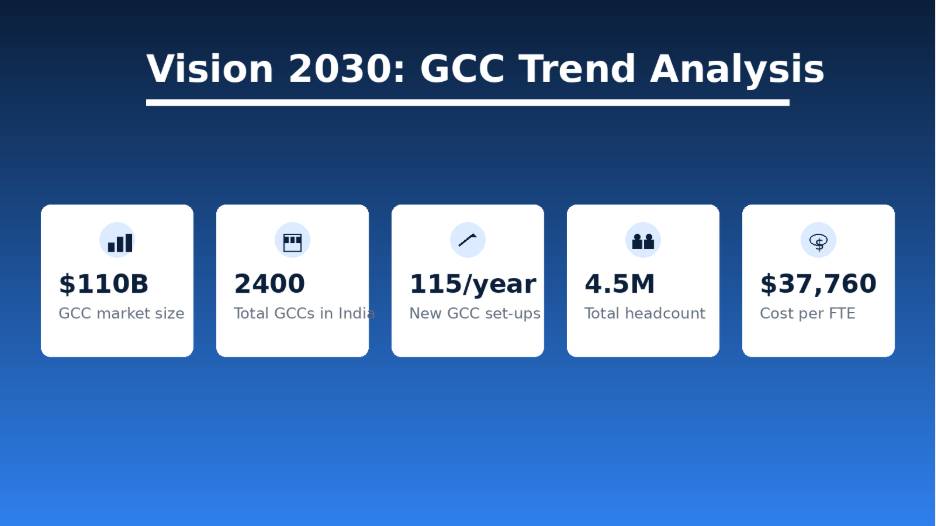

The numbers are hard to overstate. As of 2025-2026, India hosts over 1,800 GCCs, more than half of all GCCs worldwide. These centers employ nearly 2 million professionals and have generated $64.6 billion in revenue in FY2024, with direct economic output climbing to $76 billion in FY2025.

By 2030, the sector is on track to surpass $100–110 billion annually, expand to 2,100–2,400+ centers, and power a workforce of 2.5–2.8 million (some projections reach 3+ million when including indirect jobs).

In 2025 alone, GCCs accounted for 38% of all office leasing across India’s top seven cities — 31.3 million square feet, the highest ever recorded. More than 200 new GCCs have set up in just the last two years, with over 90% of activity still concentrated in Tier-I cities, but Tier-II/III locations accelerating fast, thanks to 10–35% cost advantages and fresh talent pools.

US-headquartered firms drive 70% of GCC demand. Companies like Google, Microsoft, JPMorgan, Goldman Sachs, and Walmart run some of their largest global operations out of Indian cities. And Bengaluru? With close to 950 GCC units, it’s effectively a second headquarters for dozens of Fortune 500 firms, and a global magnet for tech, ER&D, and BFSI innovation.

Long story short: With GCCs strategic repositioning, the sector is contributing directly over 1% of India’s GDP today and poised to deliver billions to overall economic growth by 2030.

What Are GCCs in India Actually Doing Today?

According to the EY GCC Pulse Report 2025, 92% of GCC leaders say their centers contribute far beyond cost arbitrage. Over 87% are taking ownership of end-to-end global processes, and 45% are shaping decisions on a global scale, making waves as integral collaborators across industries.

The functional breakdown has also shifted significantly. In FY13, only 18% of GCCs were classified as transformation hubs. Cut to 2025, that number had surpassed 50%.

GCCs in India are working heavily on advancing AI and machine learning capabilities, owning data foundations, governance frameworks, and scalable deployment. Close to 58% of GCCs are actively involved in building Agentic AI systems, and another 29% plan to write within a year. 83% are already scaling generative AI projects. So, India’s GCCs aren’t just experimenting with AI but deploying it at enterprise scale.

Another function where GCCs are shaping outcomes is R&D and product ownership. As of FY24-25, 24 GCCs have crossed $1 billion in export revenue — up from 19 the previous year. These aren’t just support centers, but full-scale product factories, handling product and platform development and intellectual property.

Talent models at the foundation of Indian GCCs are being reshaped dramatically. 71% of GCCs have active reskilling programs. More than 75% of leaders are backing organization-wide AI upskilling. The focus is shifting from headcount to skills, with rising demand for AI experts, data specialists, and domain-led roles, alongside expansion beyond Tier 1 cities into multi-city, hub-and-spoke models. So, the workforce is being built for the next decade.

Which Indian Cities Are Leading the GCC Shift?

India’s GCC ecosystem is expanding beyond metros and making inroads in smaller cities. Here’s a look at how Indian cities are stacking up across three distinct tiers of GCC growth.

Tier-1 Cities: The Established Powerhouses

- Bangalore (#1 GCC Hub): Bengaluru remains at the centerstage of GCC growth in India, housing over 34-39% of all GCC activity, a deep ER&D talent base, and a government that launched India’s first dedicated GCC policy targeting 500 new centers by 2029.

- Hyderabad (Fastest Growing): Second to Bengaluru is Hyderabad, effectively powering the GCC momentum. With 355+ centers, state-backed AI initiatives like T-AIM (Telangana AI Mission), and 940+ startups under its belt, the city is now the fastest-growing GCC cluster in the country.

- Mumbai & Chennai: Mumbai and Chennai are emerging on the map as Tier-1 GCC cities with specialized depth. Mumbai leverages its status as India’s financial capital for BFSI, FinTech, and corporate services. Chennai, on the flip side, has an edge in automotive, manufacturing, IT/ER&D, healthcare, and renewable energy, drawing engineering-heavy mandates with strong STEM talent and cost advantages.

Tier 2 & 3 Cities: The Rising Contenders

- Pune (Mature, High-Capacity Home to GCCs): Pune, as the engineering and automotive powerhouse, consolidates its position as the GCC hub in India with 360+ operational centers today and a clear trajectory to cross 500 centers by 2030. Home to landmark operations from behemoths like Microsoft and BMW Group, Pune excels in ER&D, industrial software, automotive tech, and enterprise SaaS. Low TCO, talent stability, and the presence of mature micro-markets make it a promising alternative.

- Coimbatore, Ahmedabad, Jaipur, Indore, Kochi, and Visakhapatnam: These cities are attracting GCC investments in lumpsum. These cities offer 10–35% lower operating costs, 10–12% lower attrition than metros, superior quality of life, and fresh talent pools.

GCC hiring in Tier-2 locations grew 21% YoY in 2025 (nearly double the metro pace), and projections show Tier-2/3 cities could host close to 39% of the national GCC workforce by 2030. Early movers are already setting up specialized centers in IT, fintech, engineering, and shared services, signaling the next wave of balanced, resilient growth.

Which Domains Are Driving GCC Growth in India?

GCC growth in India is increasingly domain-led, with Technology and BFSI at the forefront of this shift. Technology GCCs, contributing nearly 40–45% of the total landscape, have moved far beyond engineering support. They now function as core product and innovation hubs, building AI/ML capabilities, cloud-native platforms, and cybersecurity systems. These centers are deeply embedded in global product lifecycles, often owning end-to-end development.

BFSI GCCs, forming 20–25% of the ecosystem, have undergone a similar transformation. Once focused on transaction-heavy back-office operations, they now drive high-impact, decision-centric functions such as risk modeling, fraud detection, regulatory compliance, and digital banking platforms. With increasing reliance on data and real-time insights, these GCCs play a critical role in shaping financial decision-making globally.

Across both domains, the broader transition is unmistakable. GCCs are moving from execution to ownership—taking charge of platforms, products, and enterprise-critical processes. As AI, data, and digital capabilities become central to business strategy, GCCs in India are evolving into hubs of innovation and intelligence, let alone efficiency.

Is India’s GCC Boom Maturing or Just Getting Started?

GGCs began as an instrument for cost savings but evolved into strategic centers of innovation on a global scale. But growth at this measure doesn’t stay simple for long. The model is evolving, and so are the rules of the game.

- Talent is deep, but specialization is tightening: As GCCs expand, talent dynamics are becoming more complex. While India continues to offer a deep and diverse talent pool, demand for specialized skills, particularly in AI, advanced engineering, and leadership, has picked steam. Retention and capability-building are now active areas of focus, prompting many GCCs to look beyond traditional metro hubs and invest in Tier-2 and Tier-3 cities.

- Cost structures are becoming more nuanced: Cost structures, too, are gradually evolving. In major hubs, rising costs and infrastructure pressures are nudging organizations to rethink location strategies and operating models (less as a constraint, and more as a trigger for diversification.

- Performance is measured by impact: Traditional metrics like cost per FTE and utilization are no longer enough. Increasingly, GCCs are being evaluated on enterprise impact: how they contribute to revenue, accelerate innovation, improve speed-to-market, and manage risk. This transition is unlocking greater strategic opportunities, even as it raises the bar for performance.

What GCCs Actually Track Today?

- Delivery: Cycle time, automation rate, SLA compliance.

- Talent: Retention, time-to-productivity, eNPS.

- Innovation: PoCs scaled, IP impact, value realized.

- Business Impact: Revenue enabled, OKR alignment, stakeholder satisfaction.

- Risk: Cybersecurity posture, audit scores.

- Ownership is increasing, so are expectations: There are also subtle shifts underway in governance and decision-making. As GCCs take on more ownership, there is a growing need for clearer decision rights, stronger accountability, and more confident engagement with global stakeholders. Many organizations are already making progress here, though the journey is still evolving.The next phase of GCC growth in India will likely be defined by how effectively organizations balance scale with strategic depth: strengthening leadership, embedding AI-led operations, and aligning more closely with business outcomes. India’s GCC story, in that sense, is no longer just about how big it can get, but how far it can go in driving meaningful, enterprise-wide impact.

What’s Next for GCCs?

GCCs in India have already proven their ability to innovate. The next question is whether they can lead.

The shift toward being “global control centers” or “second headquarters” signals a new layer of transformation: one where GCCs move beyond building capabilities to influencing enterprise direction and leadership. This includes owning strategic priorities, driving cross-market decisions, and aligning closely with business outcomes at a global level.

In this model, GCCs are not just executing but prioritizing innovation, defining where investments go, which technologies scale, and how quickly organizations respond to market changes. They are making significant moves for leadership, governance, and alignment functions.

For enterprises, this represents a fundamental change in how global operations are structured. For GCCs in India, it marks the pivot from being CoEs to indispensable drivers of enterprise strategy.

How Infojini Can Help You Build a Future-Ready GCC

Building a GCC that delivers on the innovation promise requires more than just setting up an office and hiring engineers. It requires the right talent and infrastructure to work in tandem. That’s where Infojini comes in.

As a digital transformation and staffing company, Infojini brings the market intelligence, technology strategy, infrastructure capabilities, and workforce solutions that help establish and transform a GCC into a high-capacity innovation hub. We enable high-performing, agile delivery teams that offer comprehensive, end-to-end GCC setups. They design, build, and operate GCCs, from the first feasibility call to a fully running innovation center.

Our services include: GCC advisory and strategy, location selection, operating model design, governance frameworks, talent acquisition, Build-Operate-Transfer models, and managed services after launch.

So, whether you’re setting up your first GCC in India or scaling an existing one, Infojini’s acts as one partner, bringing the market knowledge and talent networks to make it work — faster, and with less friction.

Book a Free GCC Strategy Session